On a visit to Romania two years ago a Christian dentist explained

to me how the world economic system worked.

On a visit to Romania two years ago a Christian dentist explained

to me how the world economic system worked.

‘It’s like this,’ he said.

‘The average American earns $20 an hour and spends $25 an

hour.'

'The average Chinese man earns $5 an hour and spends $4 an hour and lends the other dollar to the American.’

'The average Chinese man earns $5 an hour and spends $4 an hour and lends the other dollar to the American.’

‘Because there are about five times as many Chinese men as

Americans the sums work out pretty well.’

‘The only problem though is that both American and Chinese man are doing the same job

and it is a global market.'

'So what will happen in time is that wages in America will come down and those in China will go up and when that happens there will be an awful lot of kicking and screaming in the US and possibly something even worse.’

'So what will happen in time is that wages in America will come down and those in China will go up and when that happens there will be an awful lot of kicking and screaming in the US and possibly something even worse.’

I haven’t checked his sums but I thought his comments were

rather insightful and the general gist

is chillingly correct.

We all know that US debt is spiralling out of control, but

all we get from the media is a moment by moment commentary but without the big

picture.

So the Telegraph tells

us today that Washington is due to hit its borrowing limit on 17 October,

at which point the US government runs out of ‘extraordinary measures’ to raise

new cash to pay its bills, risking an unprecedented default on US sovereign

debt.

We are warned that markets are therefore braced for a choppy

week because US politicians failed to strike an agreement on raising the debt

ceiling over the weekend, leaving it just days away from hitting its

$16.7 trillion (£10.3 trillion) borrowing limit.

Jim Yong Kim, President of the World Bank, on Saturday has warned

that the US is just ‘five days away from a very dangerous moment’ unless

politicians produce a plan to avoid default.

Christine Lagarde, President of the IMF, meanwhile repeated

her warning that failure to raise the US borrowing limit would lead to ‘massive

disruption the world over’.

Christine Lagarde, President of the IMF, meanwhile repeated

her warning that failure to raise the US borrowing limit would lead to ‘massive

disruption the world over’.

But let’s put the daily headlines aside and look at the big

picture.

By raising the debt ceiling even further the US will be

moving even more into unprecedented debt.

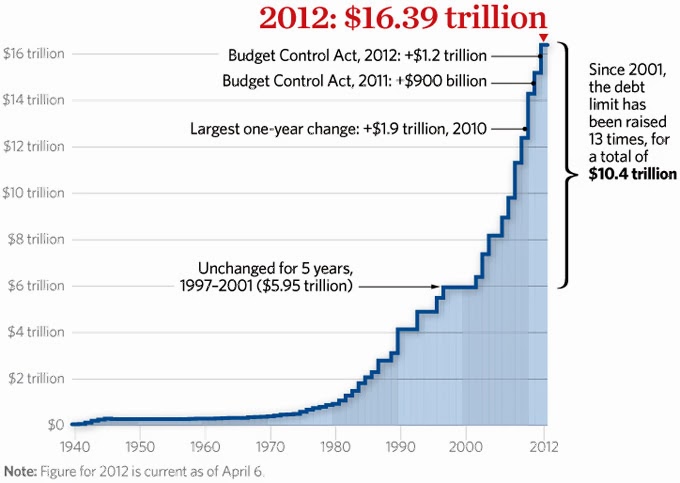

Since 2001 the debt limit has been raised 14 times for a

total of $10.7 trillion to its present level of $16.7 trillion (see above).

It also stands at around 100% of GDP, the highest level

since the Second World War (see right).

It also stands at around 100% of GDP, the highest level

since the Second World War (see right).

So who is this debt owed to? (see below)

Over half of the debt is publicly owned within the US or is

tied up in Social Security Trust Funds.

Over 30% is owed abroad with China (8%) and Japan (6%) being

the biggest creditors.

When I was a boy my father taught me to live simply, give

generously, save for future necessities and never to go into debt. It has

served me well.

St Paul told the church in Rome to ‘Let no debt remain

outstanding, except the continuing debt to love one another.’ (Romans 13:8)

Jesus was even more radical, ‘Give, and it will be given to

you. A good measure, pressed down, shaken together and running over, will be

poured into your lap. For with the measure you use, it will be measured to you.’

(Luke 6:38)

Why is it I wonder that the richest nation on earth is also the

most indebted and lurching from one financial crisis to another?

Why is it I wonder that the richest nation on earth is also the

most indebted and lurching from one financial crisis to another?

I suspect the answer is found in another Bible book, ‘Human

desires are like the world of the dead - there is always room for more.’

(Proverbs 27:20)

However high your income is, if your expenditure is greater

you are heading eventually for a fiscal cliff without a happy landing.